If there is one industry that continues to boom in the UK, it is the gambling sector.

In the year ending 2016, Britain’s gambling sector generated turnover of £13.6 billion, underlining the fact that the UK operates one of the most progressive and lucrative markets in the world. While online casino growth dominates this market, it is also fair to surmise that some aspects of land-based gambling are also continuing to thrive, as the market continues to benefit from increased regulation and pronounced diversification.

In this article, we will chart the course of the UK’s gambling industry in numbers between 1999–2017, while striving to identify key trends for the future.

A Brief Background

The history of gambling in the UK is an interesting one, although it was in the early 1900s that two Royal Commissions were established to determine the practice could be regulated to reduce crime and drive government tax revenues. This was a progressive outlook at the time, while their recommendations ultimately to the legalisation of betting in licensed betting shops and casinos under government supervision in the 1960s.

The mid-nineties triggered a significant shift in the marketplace, however, after the establishment of the National Lottery in 1994 and the emergence of online gambling in 1996. This created tremendous growth within the industry, while also gradually propelling gambling into the consumer mainstream. Since the late 1990s, the industry has continued to enjoy considerable growth, while there is no sign that this is likely to abate any time soon.

1999–2007: The Diversification of the UK’s Gambling Market

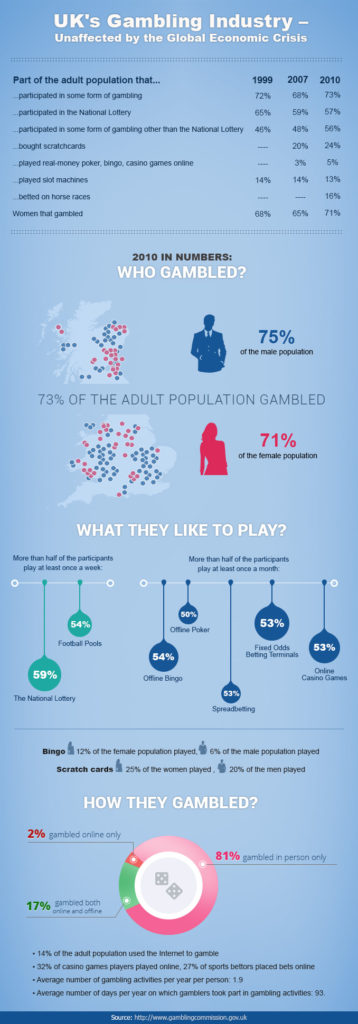

Back in 1999, the evolution within the UK’s gambling market was just about to begin in earnest. At this time, the National Lottery was at the peak of its popularity, with an estimated 65% of the adult population participating in this on a regular basis. Despite this, just 46% of the UK’s eligible population engaged in gambling activities at the turn of the century, with the burgeoning online market yet to become immersed in the consumer mainstream.

Similarly, creative gambling products such as scratch cards had yet to be embraced, contributing to a popular and yet restricted market that lacked diversity.

The next eight years changed this, however, as while the level of participation in the National Lottery declined to 57%, scratch cards, online slots and virtual casino gameplay increasingly popular. 20% of the adult population regularly purchased scratch cards by 2007, for example, while 17% indulged their passion for slots and video poker. Overall, this caused the number of adults who gambled in the UK to rise to 48%, as the market continued to evolve, become more accessible an cater to a wider array of needs.

While the level of growth in the market was steady rather than spectacular between 1999 and 2007, it was tangible and reflected increased diversification in the sector. This was aided in part by the Progressive Gambling Act of 2005, which enabled land-based and online gambling brands to advertise so long as they included measures to address the issue of problem gaming. This was key, as it allowed brands to invest heavily in the promotion and laid the foundations for more pronounced growth in the future.

2007–2010: The Start of Sustained and Exponential Growth

It was in September of 2007 that the Gambling Act of 2005 came into law, and this remains a seminal point in the history of the market as a whole. At the time, the industry was worth an estimated £91 million, while it was benefiting from the type of consistent growth that had seemed unlikely at the turn of the century. The new legislation would major brands embark on huge promotional campaigns, however, as they looked to target new customers with increasingly tailored and unique gaming experiences.

This took hold over the next three years, and by 2010 the rate of growth was already reaching epic proportions. 73% of all UK adults participated in one form of gambling or another at this time, for example, while 71% of female customers also engaged with the pastime.

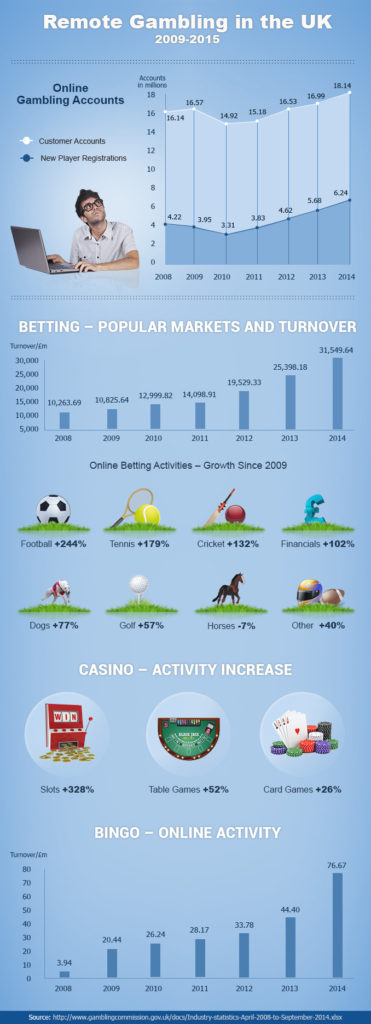

The interesting point to note here was that offline gambling remained the dominant channel at the end of 2010. Just 2% of the population gambled solely online at this time, while a staggering 81% would only gamble in bricks-and-mortar establishments. This was also the last year that the number of active online casino dropped, falling from 16.57 million in 2009 to just 14.92 million. There were gradual signs that this trend was about to reverse, however, with 17% of gamblers embracing online platforms with a view to making a transition and a rising number of casino games (32%) being played in the virtual realm.

2010–2017: How UK Gambling Became a Thriving (and Increasingly Remote) Marketplace

This trend has certainly continued at pace, reaching a head in 2016 when online gambling was established as the primary driver of growth in the overall market. Despite this, it is incredible to note that most forms of bricks-and-mortar based gambling have also recorded increased growth during the same period, highlighting the fact that virtual gaming has popularised a number of games while creating a unique opportunity for cross-platform interaction.

In terms of numbers, however, it is the growth of online gambling that has been most impressive since 2017. The number of online gambling accounts have increased incrementally since the aforementioned dip in 2010, for example, reaching 18.14 million by the end of 2014. The increase in the rate of new player registration has been even more pronounced nearly doubling in just four years between 2010 and 2014, while there were a total of 21.57 million active gambling accounts online at the end of 2015.

In the virtual realm, the biggest areas of growth remain sports betting and casino games. The former has seen astonishing growth online since 2010, when brands generated £12.99 million from sports wagers. This had more than doubled by 2013, while the following year saw this niche generated cumulative revenue of £31.54 million. The following year, punters wagered a record £9.518 billion on sporting events, with football the single most popular pastime and estimated to have generated £449.44 million in bets.

Interestingly, online wagers have increased by a staggering 244% since 2010, while tennis (179%), cricket (132%) and financials (102%) have also enjoyed treble digit growth. In fact, only horse racing has seen a noticeable decline in terms of the value of online bets, having fallen by 7% over the course of the last seven years (which has much to do with the popularity of high street bookmakers and live betting) among fans of the sport.

Online casino and bingo gameplay have seen similar growth since 2010, with virtual slots embodying this better than any other pastime. Not only do slots now account for an estimated 80% of all online casino revenues, for example, but this niche has seen an activity increase of 328% during the last seven years. So even though table and card games have enjoyed increases of 52% and 26% respectively, it remains clear that the diversification of slots has made them a key driver of success in the modern age.

Not only this, but the emergence of independent comparison sites has also helped to build trust between brands and customers, creating the potential for longer consumer life-cycles and superior margins.

Then we come to online bingo, which generated revenue of £26.24 million back in 2010. This had nearly trebled to a staggering £76.67 million in 2014, as players abandoned their local halls and began to operate virtually on the back of a mass television advertising campaign by various brands. 2016’s figures suggest that online bingo generated an estimated £153 million, highlighting the incredible growth that has gripped the sector for the best part of a decade.

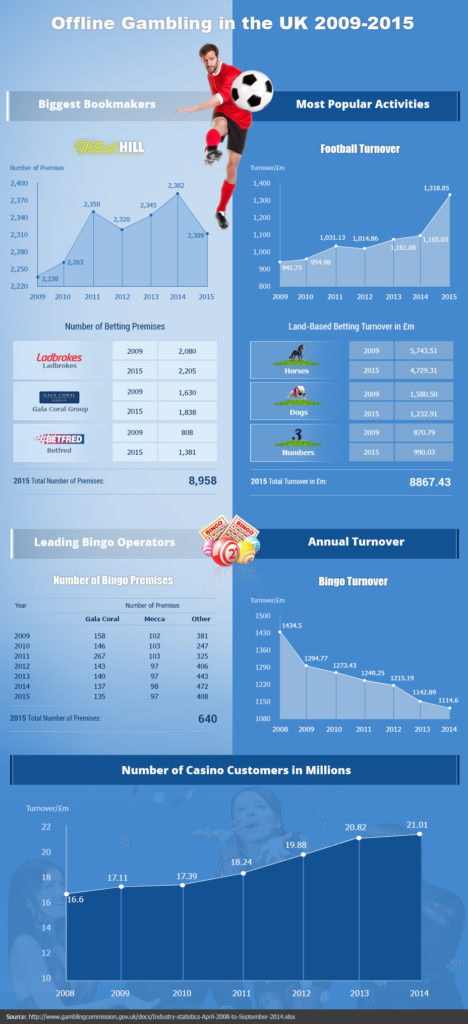

The growth of the virtual bingo market offers a natural segue-way into the world of land-based gambling. After all, we have already touched on the fact that many aspects of this market continues to enjoy robust growth, although admittedly at a far slower rate than their online counterparts. The one exception to this rule is the bricks-and-mortar bingo industry, however, which saw annual revenues decline from £1.4 billion in 2010 to just £1.1 billion four years later.

This rate of decline has continued, making it likely that online bingo will generate more income than land-based sites within the decade.

The decline of offline bingo is an exception to the general rule, however, with the number of bricks-and-mortar casino visitors actually increasing between 2010 and 2014. Land-based establishments boasted 16.6 million returning customers seven years ago, but this rose to an impressive 21.01 million in just four years. Clearly this rate of growth is steady than the one that drives the online marketplace, but there is still demand for increasingly diverse casino establishments that strive to integrate technology into their outlets.

READ: 5 Places Every Poker Player Must Visit While in London

The same trend can be seen in offline sports betting, which continues to see its revenues grow despite intense competition from virtual competitors. Greyhound racing wagers saw an estimated revenue increase of $347 million between 2010 and 2015, for example, while land-based football betting grew at a similar rate (from £954 million in 2010 to £1.3 billion five years later). These continue to be impressive numbers, which highlight the level of demand that remains for traditional gambling channels in the digital age.

The Last Word: The Future Trends in the UK Gambling Industry

As these figures show, there are several trends that define the real-time gambling industry in 2017. Some of these will come of no surprise, of course, such as the growth of online gaming and its growing influence as a revenue generator in the sector (it accounted for 33% of all turnover at the end of 2016).

The robust performance of most land-based gambling activities will surprise many, however, as it is logical presume that the rise of online gaming would sound the death knell for the traditional market. While this may have been true in some industries, the gambling industry has actually seen innovation popularise a host of casino and betting activities by propelling them into the mainstream, creating heightened demand for both off and online experiences.

So what does this tell us about the future?

In short, we should expect the rise of online gaming to continue at pace, as it continues to evolve and diversify to meet an ever changing demand. Over the course of the next decade, we may also see the online gambling share approach 50% of the market, while mobile gaming playing an increasingly seminal role in this.

During the same period, the level of offline activity is also likely to grow incrementally. The rate of growth in this sector will become gradually slower, however, as generational and technological shifts force more players online and trigger a decline in demand for traditional gaming. We may then see land-based casinos and sports betting hubs experience a similar decline to land bingo halls, as online gambling finally leverage their full potential and come to dominate the industry.

So, high street bookmakers have arguably begun to prepare for this, by reinforcing their online presence and closing some of their physical stores. This will certainly be something to watch with interest in the future, as this most fascinating of markets continues to evolve at a truly incredible pace.

Comments